China's recovery from the pandemic

- blog de anegrete

- 4301 lecturas

The outbreak of COVID-19 began in China at the end of December 2019, the quarantine and lockdown were in January, and the social distancing initiated in March 2020. These health provisions reverted the national economy for the first time in almost three decades. They pushed some Global Value Chains out of business, mainly pharmaceuticals, automobiles, aeronautics, electronics, and telecommunications. Faced with the problem, the Chinese Government immediately implemented policies to hold the economy from collapsing. What happened to the economy during the pandemic? Has it recovered?

Xi Jinping's administration has been on the job to combat COVID-19 since January 2020. Since late January, his Government's policy initiatives have mainly focused on health, such as constructing new hospitals, health care goods production, and quarantine measures. The people's health care holds a sizeable economical cost, chiefly since production ground to a halt. The Ministry of Finance immediately used fiscal policy instruments and the Central Bank monetary ones to cushion the fall.

From February through to August this year, the Central Bank placed 5.8 billion yuan with open market operations. The measure intended to maintain the liquidity of the banking system during the pandemic. The first and largest monetary policy stimulus package occurred in February, with 1.7 trillion yuan allocated to strategic companies. Medical supply manufacturers received credit lines, as did SMEs and agricultural companies as well. Finally, there was a one-year bank loan payment deferment until March 2021.

As for fiscal policy, the Ministry of Finance injected 4.5% of GDP on May 28. This package went for unemployment insurance, infrastructure, and price subsidies. Other budgetary provisions included tax deferrals for small and family businesses and exemptions for households from value-added taxes. These shots helped the country's macro-economy and kept poverty at bay when the rest of the world has growing poverty.

Over the past three years, the economy had an average of 6,4 per cent growth per quarter annualised, but it fell by -7 percent in the first quarter of 2020. It was a -13,4 percent turnaround and the country's foremost economic contraction in nearly three decades. However, the second quarter of 2020 already observed an impressive 3% growth with a V-shaped recovery in the making. Economic policy actions certainly cushioned the fall. Timely fiscal and monetary stimuli did not allow for a more considerable drop in consumption and investment within the country.

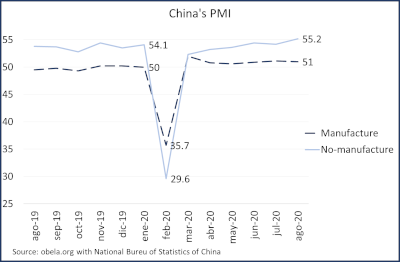

The purchasing manager's index (PMI) shows the macroeconomic situation based on companies' surveys on production, employment, foreign trade, and new orders. When the index is over 50, the economy is expanding, and when under, it is contracting. There exist two PMI's, a manufacturing and a non-manufacturing one, and both collapsed in February, reaching the first one reaching 35.7 and the second 29.6. The collapse of the last one was more dramatic, given unemployment in services. It is remarkable that they are both now above their pre-summer level. The non-manufacturing sector is on a faster upward trend.

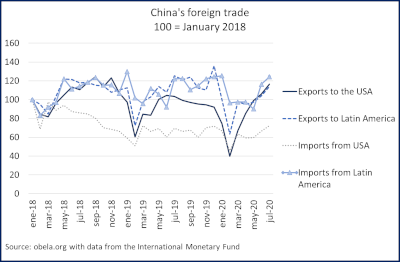

International trade also shows a fall and a recovery. Chinese exports to the whole world fell dramatically in February when the world economy entered a recessionary state. However, exports to Latin America, bounced back in March and are still on an upward trend, not reaching yet the levels previous to the pandemic. Meanwhile, Latin American imports never fell radically given they are raw materials such as soya, copper, meat, and other types of minerals.

What is thought-provoking is the Asian giant's trade with the USA. After an agitated two years due to the trade war, a formal agreement was reached in January 2020 to cease hostilities. The result is that China's trade with the US is reduced on the import side; that is, the Asian partner is no longer buying as much from the US, with the pandemic having further deepened the trend. Surprisingly exports observed a very marked "V" shaped recovery, unexpectedly bringing in an even more massive US trade deficit with China than before the war. The US sells less and buys more from this economic giant at the end of two years of a trade war. The trade war has not changed the US purchasing pattern, and so, according to the US Census, it now has a more massive deficit than in 2018.

Finally, there is a Chinese economy recovery in terms of GDP and PMI. The immediate and correct economic policy actions have mitigated the fall and boosted the recovery. Its trade dynamics are also recovering, and in particular, exports to the US are burgeoning. Currently, the Asian country's economic dynamics is not induced by international trade but rather by the domestic market, making it the only country globally with a reliable V-shaped recovery with annualised quarterly real growth in 2020. Governments wishing to grow or not decline so much will have to look at it closely.