Covid-19: the beginning of the domino effect

- blog de anegrete

- 4259 lecturas

The effects of COVID-19 on the real economy are beginning to materialize around the world. Starting in the second half of March, the first signs of the deterioration of confidence and uncertainty occurred with the world's major stock market indices falling to multi-year lows; for example, the Dow Jones dropped to the 2016 level, the Frankfurt DAX to 2012, and so on. This note presents labour, industry, and services sector indicators for the G7 and BRICS economies. The same situation is reflected in the rest of the world, with a drop in output and international trade and massive unemployment despite the efforts of economic authorities to inject liquidity. The massive injections of cash by the central banks of the US, UK, European Union, and Japan are helping banks to invest that money in the stock markets and thus try to stabilise them. Meanwhile, the Chinese stock market remains stable.

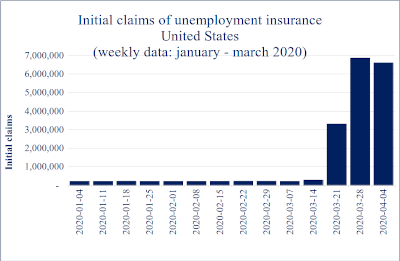

The weekly Unemployment Insurance Claims (SND) indicator from the US Department of Labor shows that historically the levels are around 300,000 unemployed people with insurance. This figure dropped to 218,000 during 2019 and ended in the second week of March when there was a slight increase. In the third week of March 2020, unemployment insurance claims increased 15-fold to 3,307,000; in the fourth week, 6,867,000; and the last available data from the first week of April was 6,606,0001; with a record 17 million people unemployed in three weeks. California, New York, Michigan, Florida, and Georgia are the states with the most confirmed cases and the same ones with the most unemployment insurance claims. As the number of states with higher case volumes expands, those claims will grow by business closures.

The service sector is the most affected, mainly in recreational activities and in food and bar services. To a lesser extent, professional and business services are affected, as well as retail trade and construction. Given the speed with which activities have come to a standstill and the likely bankruptcy of small and medium-sized businesses and enterprises, there is no prompt recovery of the jobs lost. It will be a slow recovery giving the economic crisis a U-shape or, in the worst-case, L-scenario. It will not have a V-shape, with a rebound, unlike 2009. The difference between the U and L is the period the economy will remain stagnant. During that time, new economic activities take place with a complete shift of the energy matrix from oil to clean energy.

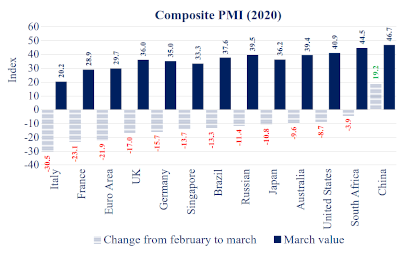

The Purchasing Managers' Index (PMI) published by the IHS Markit indicates the expectation of the situation in various economic sectors ahead of traditional macroeconomic indicators. There are three primary levels: manufacturing, services, and composite. The graph shows the composite PMI of the G7 countries plus the BRICS, for March, and the variation from February to March of this year. A level below 50 represents a contraction. Evidence shows it is the case for all economies presented, with Italy, France, and the United Kingdom observing the most significant drops. The fall in the services PMI is more significant than those shown in the manufacturing PMI.

The only country with a V-shaped economic crisis was China. It bounced back from 27.5 in February to 46.7 in March. The global domino effect began in February in China and spread to the rest in March. What precipitated the domino effect was the global value chains that have manufacturing in China as their starting point, closed in January and February. Then there is the powerful effect of the spread of COVID-19. The closure of businesses and the paralysis of economic activity in the world explains the worse impact on the PMI of the service sector.

The difference between the COVID-19 crisis and that of 2008 is the degree of penetration since it covers all sectors and socio-economic levels around the world. In a context of a recessionary world economy that was pointing downwards, productive paralysis unleashed. The dangerous thing is that until there is a cure and it becomes massive, the crisis may have consequences not seen since the Great Depression of 1929, according to statements by the managing director of the IMF. Meanwhile, with the epidemic under control, China recovers through internal value chains with a strong role of the state in the economy.

1 https://www.dol.gov/ui/data.pdf